Objective: Evaluate the feasibility and potential of Financial AI Sights to solve a specific financial query.

Scope: The concept testing will focus on the core functionality of the application, including:

- Receiving user queries through a form.

- Sending the query to the Gemini API.

- Receiving and processing the response from the API.

- Presenting the response to the user in a clear and concise manner.

Methodology:

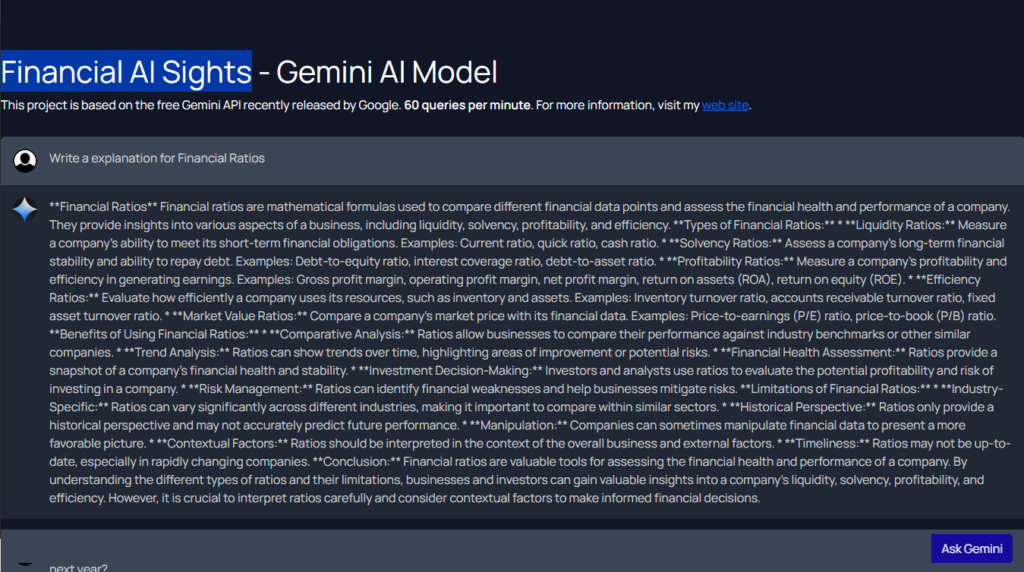

- Design the Test Case: Select a financial sample query that addresses the problem your application aims to solve. This query should be similar to what real users are expected to input in the future.

- Run the Test:

- Enter the query into the application’s form.

- Observe the application’s behavior during the process of sending and receiving information.

- Evaluate the accuracy and usefulness of the response provided by the Gemini API.

- Document your observations and test results.

- Examples:

Liquidity Ratio Analysis

Income statement summary:

Total Current Assets: $100,000

Total Current Liabilities: $60,000

Query: Write an explanation for Current Ratio. What does a current ratio of 1.67 indicate about this company's short-term financial health?Profitability Analysis

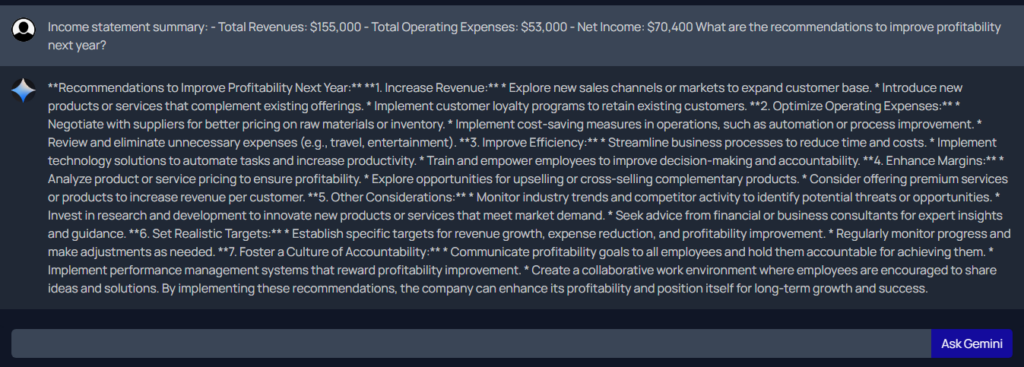

Income statement summary:

Total Revenues: $155,000

Cost of Goods Sold: $75,000

Gross Profit: $80,000

Total Operating Expenses: $53,000

Operating Income: $27,000

Query: Write an explanation for Gross Profit Margin and Operating Profit Margin. What do these ratios indicate about the company's profitability, and how can they be improved?Success Criteria:

- The application must send the query to the Gemini API without errors.

- The application must successfully receive and process the API response.

- The response from the API should be relevant to the user’s query and contain helpful information.

- The application must present the response to the user in a clear, concise, and easy-to-understand way.

Resources:

- Python Flask application.

- Access to the Gemini API.

- A test case with a sample query.

- The application will be based on a data set of IFRS financial statement definitions and other technical papers contained in JSON files.

{

"elements_of_financial_statements": {

"asset": "A present economic resource controlled by the entity as a result of past events which are expected to generate future economic benefits.",

"liability": "A present obligation of the entity to transfer an economic resource as a result of past events.",

"equity": "The residual interest in the assets of the entity after deducting all its liabilities.",

"income": "Increases in economic benefit during an accounting period in the form of inflows or enhancements of assets, or decrease of liabilities that result in increases in equity. However, it does not include the contributions made by the equity participants (for example owners, partners or shareholders).",

"expenses": "Decreases in assets, or increases in liabilities, that result in decreases in equity. However, these do not include the distributions made to the equity participants.",

"other_changes_in_economic_resources_and_claims": "Contributions from holders of equity and distributions to them."

},

"recognition_of_elements": {

"criteria": "An item is recognized in the financial statements when it is probable that future economic benefit will flow to or from an entity and the resource can be reliably measured.",

"additional_conditions": "In some cases specific standards add additional conditions before recognition is possible or prohibit recognition altogether.",

"exceptions": {

"internally_generated_intangibles": "Recognition is prohibited by IAS 38 for items like internally generated brands, mastheads, publishing titles, customer lists.",

"research_and_development_expenses": "Can only be recognised as an intangible asset if they cross the threshold of being classified as 'development cost'.",

"provisions_for_contingent_liabilities": "IAS 37 prohibits the recognition of a provision for contingent liabilities, except in a business combination where it is recognised even if an outflow of resources embodying economic benefits is not probable."

}

},

"concepts_of_capital_and_maintenance": {

"financial_capital_maintenance": "A profit is earned only if the financial amount of the net assets at the end of the period exceeds the financial amount of net assets at the beginning of the period, after excluding any distributions to, and contributions from owners during the period.",

"physical_capital_maintenance": "A profit is earned only if the physical productive capacity of the entity at the end of the period exceeds the physical productive capacity at the beginning of period, after excluding any distributions to, and contributions from owners during the period."

},

"requirements_of_IFRS": {

"presentation_of_financial_statements": {

"statement_of_financial_position": "A balance sheet.",

"statement_of_comprehensive_income": "This may be presented as a single statement or with a separate statement of profit and loss and a statement of other comprehensive income.",

"statement_of_changes_in_equity": "",

"statement_of_cash_flows": "",

"notes": "Including a summary of the significant accounting policies."

},

"general_features": {

"fair_presentation_and_compliance_with_IFRS": "Requires the faithful representation of the effects of the transactions, other events, and conditions.",

"going_concern": "Financial statements are presented on a going concern basis unless otherwise indicated.",

"accrual_basis_of_accounting": "Recognise items as assets, liabilities, equity, income, and expenses when they satisfy the definition and recognition criteria.",

"materiality_and_aggregation": "Every material class of similar items has to be presented separately.",

"offsetting": "Generally forbidden in IFRS, except when specific conditions are satisfied.",

"frequency_of_reporting": "At least annually a complete set of financial statements is presented.",

"comparative_information": "Comparative information is required in respect of the preceding period for all amounts reported in the current period's financial statements.",

"consistency_of_presentation": "The presentation and classification of items in the financial statements are retained from one period to the next unless a change is justified."

}

}

}Expected Outcomes:

- The concept testing should demonstrate the application’s ability to receive a user query, send it to the Gemini API, and effectively present the response.

- The information provided by the Gemini API should be valuable to the user and contribute to decision-making.

- The concept testing should identify areas for improvement to optimize the application’s performance and usability.

Evidence:

- A record of the conducted tests, including the queries used, API responses, and observations on the application’s behavior.

- Screenshots or videos documenting the interaction process with the application.

Conclusions:

- The concept testing will determine if the application has the potential to solve the intended problem.

- This will help identify the application’s strengths and weaknesses in its current state.

- You’ll gain recommendations to enhance the application’s functionality and user experience.

Next Steps:

- Refine the application based on the concept testing results.

- Implement the identified improvements to optimize performance and usability.

- Conduct additional testing with various cases to ensure the application’s robustness.

- Consider the application’s scalability for future use with a larger number of users (Cloud Platforms and containers).

Additional Recommendations:

- Involve potential users in the concept testing to gather feedback and suggestions.

- Document the testing process and results in detail.

- Share the concept testing results with stakeholders to gain their support and funding for further development.